Find out the latest global market share numbers and trends for major cloud providers, including AWS, Azure, GCP, Alibaba, Oracle, IBM, and more.

The modern cloud computing market first emerged in 2006 with AWS S3 and EC2. Amazon founded these services following its own struggles with speed and scale. Almost two decades later, the cloud computing market is now worth a whopping $855.7 billion. It’s steadily growing still, at a compound annual growth rate (CAGR) of 18.91%. According to public cloud market reports, the market size is expected to grow to $1.76 trillion by 2029, at a CAGR of 21.4%.

Cloud market share is an important factor to consider when comparing cloud service providers (CSPs). To make it easier, we’ve gathered and analyzed the cloud market share of top cloud computing and infrastructure service providers, all in a single place. Continue reading to find out where cloud market shares of major CSPs stand as we head into 2026.

Given Amazon’s early entry, the biggest chunk of the cloud computing market has always belonged to AWS. Other cloud computing leaders, like Microsoft Azure, Google’s GCP, Alibaba Cloud, Oracle, and IBM, have also claimed significant shares. Despite hyperscalers owning a disproportionate share of the cloud market, the market is slowly becoming more diverse and fragmented, with smaller and niche players reporting promising year-over-year growth and challenging hyperscalers’ monopolies.

Hyperscalers have undeniably proven their worth and resilience, honed their infrastructure, expanded their service portfolios, and maintained customer trust over the years. However, as we’ve discussed in our recent review of the top 10 CSPs, smaller, niche players are often better suited for certain workloads, use cases, and businesses.

In order to balance the scale and reliability of hyperscalers with the flexibility and specialization of niche cloud providers, you can opt for a multi-cloud strategy. Choosing a strategic combination of various cloud providers can improve your organization’s resilience and allow you to maintain control over your cloud landscape as your cloud needs evolve.

emma, cloud management platform, helps you tap into the capabilities and benefits of any number of cloud service providers without having to deal with their underlying differences. It lets you manage all cloud environments from a single visibility and management dashboard, eliminating the usual complexities of managing a multi-cloud. You can centrally optimize your cloud configurations and freely migrate or scale workloads across heterogeneous cloud environments, without running into interoperability and incompatibility issues.

As a result, you can easily choose multiple cloud providers, for instance, hosting mission-critical workloads on experienced hyperscalers while still being able to experiment with ground-breaking, specialized offerings of newer entrants and challengers. By choosing various cloud providers for your different business needs, you can maximize cloud benefits and maintain your cloud freedom.

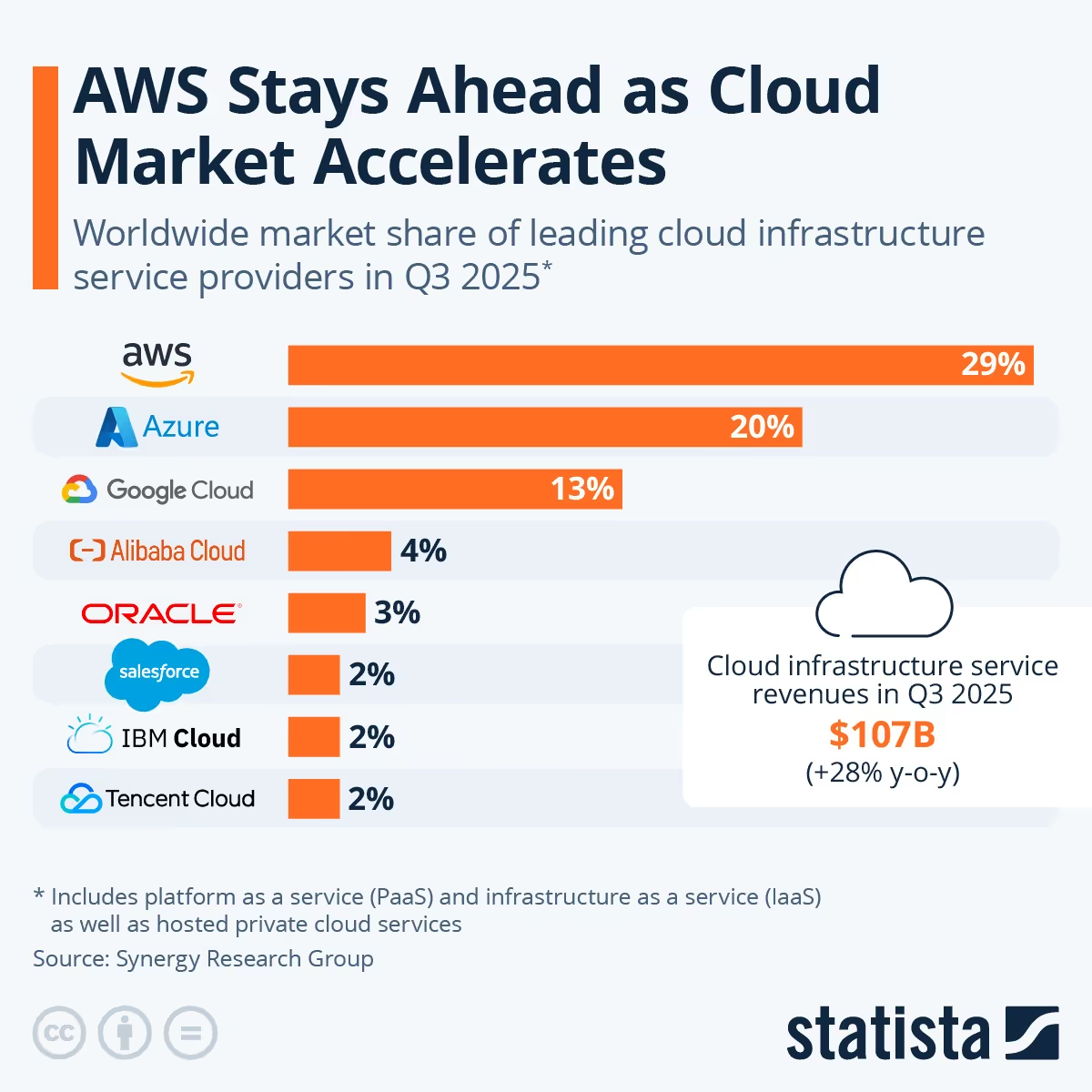

AWS remains the leader, primarily because of the sheer range of its cloud services. It offers over 200 fully-featured services. However, this breadth of services can sometimes come at the cost of depth. Perhaps that’s why it’s slowly losing ground to some other competitors.

AWS’ market share has seen a slow but consistent decline: from about 33% in late 2021 to 32% in Q1 2023, and down further to 29% by Q3 2025. This recent decline in market share after years of being an uncontended cloud leader shows how cloud competition is getting fiercer every year. In order to capture a slice of the AWS-dominated market, other vendors have strategically focused on areas where AWS is perceived as lacking. For instance, Azure targets hybrid cloud, while GCP excels in data analytics and AI. On top of that, players like IONOS and OVHcloud are becoming increasingly attractive for organizations prioritizing data residency and regulatory alignment.

AWS got the largest slice of the cloud computing market due to its early-mover advantage. Still, Azure has been managing to surpass AWS in growth for years now. Even in Q3 2025, Azure’s 21% Y-o-Y growth surpassed AWS despite the latter bringing in more revenue.

This is because Azure has its ecosystem of Microsoft products (e.g., Office 365, Teams) to its advantage. Combined with a strong hybrid cloud portfolio (Azure Arc, Azure Stack), enterprises often lean towards Azure more than AWS. Despite strong enterprise demand, Azure’s market share has slowly dropped from 24% in 2022 to 20% in 2025, likely due to the rise of niche players.

GCP’s market share was at its peak at 9.5% in 2019. It fell slightly over the next couple of years to 7%, until the AI revolution happened. Now GCP has reclaimed most of its lost ground mainly because of its customizable and easy-to-use AI/ML offerings.

Alibaba Cloud’s global market share was at 6% in 2020, which dropped to a meagre 4% by Q4 2024. Over the past few years, Alibaba has faced a huge decline in its international market due to the geo-political tensions and US-imposed curbs on chip exports to China.

Within China though, Alibaba Cloud is still the leading cloud player with a 36% market share. It’s one of the top choices for Chinese and APAC businesses because of its localized support, compliance, and deep integration with Alibaba’s e-commerce platforms.

Businesses already using Oracle’s software products like databases and ERP systems often prefer OCI for its seamless integration. However, Oracle Cloud has slow adoption outside Oracle’s core customer base. OCI held a market share of around 2.8% in 2019, and is still steady at 3%.

OCI’s strong IaaS growth in the past year alone can be attributed to AI demand. Many of its new cloud contracts come from AI‑heavy customers and workloads, including deals tied to high‑performance infrastructure and database + AI‑model integrations.

Back in 2019, IBM made a strategic decision to focus primarily on the hybrid cloud market. IBM's acquisition of Red Hat led to a modest market growth, but IBM’s share has mostly fluctuated between 2-3% since then.

There is no public data showing how much of Q3 2025 revenue came solely from IBM Cloud offerings.

Tencent Cloud has a strong presence in China and Southeast Asia markets. It is also steadily increasing its datacenter footprint across Asia-Pacific, Europe, and North America. Overall, Tencent’s cloud offerings are geared toward gaming, media, and entertainment industries.

Cloud computing services are available in three primary service models:

The IaaS and PaaS markets are still dominated primarily by hyperscale giants, including AWS, Azure, GCP, Alibaba, and IBM. However, the SaaS market shares are much more nuanced and evenly distributed. Here’s what recent SaaS market shares look like:

Other notable vendors include Adobe, ServiceNow, Zoom, Shopify, Atlassian, HubSpot, Netflix, and more. Overall, when you exclude IaaS and PaaS offerings, the remaining cloud service market is much more diverse and competitive with vendors focusing more on niche offerings rather than comprehensive portfolios.

Cloud service providers’ market share trends vary widely across geographic regions:

A good cloud market share analysis can give you a clear idea of the market leaders and emerging trends. Other factors you should consider when evaluating CSPs include:

You need to evaluate all these factors comprehensively against your own business needs to find one or more providers that meet your requirements. This will ensure that you are able to form strategic partnership that is mutually beneficial over a longer term.

Not sure where to start? Read our comprehensive and actionable guide: How to Choose a Cloud Provider: 7 Key Criteria for IT Leaders.